This is one pricey market, and if you’re hesitant to put new money to work, I am sympathetic. After all, we’re here for the dividends. We want our principal to stay intact, so I understand it doesn’t make much sense buying high if we’re going to collect dividends but then watch the stock market proceed lower.

Valuations seem to have decoupled from fundamentals in many cases. As we speak, SpaceX, for example, claims an addressable market of $28.5 trillion–roughly the size of the entire U.S. economy. Which is all fair and well–but it also commands galactic premiums at 100 times sales.

I’m relatively young and healthy, but I’m not confident that I’ll be here for a hundred more years to collect those sales. As such, I’m a good old-fashioned dividend investor, and I love a deal alongside my dividend.

Let’s talk cheap stocks that pay today.

Closed-end funds (CEFs) are built differently than mutual funds and exchange-traded funds (ETFs). CEFs have a fixed number of shares, which means their prices routinely disconnect from the value of what they own.

That inefficiency is our opportunity–we can buy stellar assets at 95 cents, 90 cents, even less on the dollar.

Take, for instance, these five CEFs that are offering up sky-high 6.0% to 10.4% yields that we can buy for 4% to 14% less than what they’re actually worth.

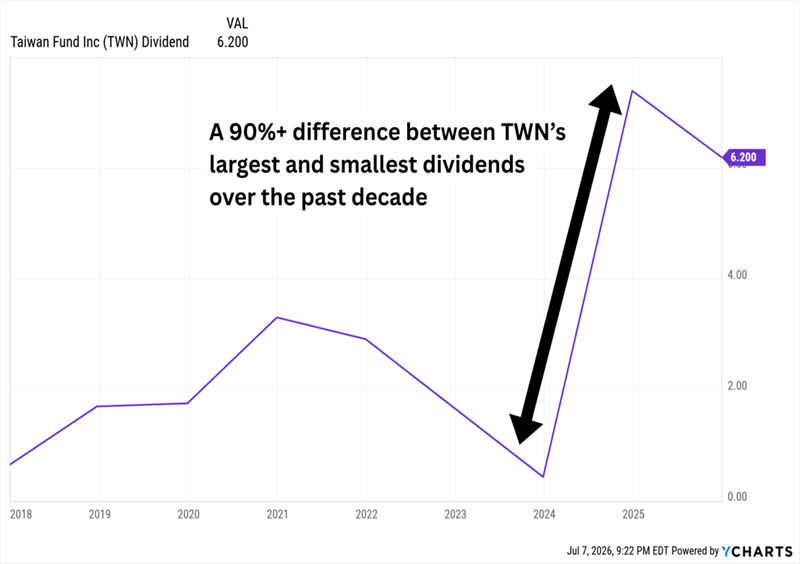

Taiwan Fund (TWN)Distribution Rate: 6.6%

The Taiwan Fund (TWN) is a perfect example of how CEFs let us buy even white-hot assets for less than they’re worth.

Nomura Asset Management’s Sky Chen is tasked with building a portfolio of stocks listed on the Taiwan Stock Exchange that represent a “broad spectrum” of the ROC economy. While it lists a number of industries, it specifically states that it “will invest more than 25% of its total assets in the semiconductor industry.”

A lot more, as it turns out. Taiwan Semiconductor Manufacturing (TSM) alone accounts for a third of the portfolio, which is stuffed with other semiconductor and technology stocks. In fact, the sector makes up 85% of assets. TWN isn’t broad, either, at fewer than 30 stocks right now.

Not That Anyone Is Complaining

Chen doesn’t use leverage or options–just a concentrated portfolio that pays out a substantial, if wildly variable, annual distribution. Right now, that sky-high distribution reflects the portfolio’s ludicrous gains, but that hasn’t always been the case.

Like Many International Single-Country CEFs, Distributions Are a Crapshoot

Despite TWN’s rocketship returns, the fund still trades at a 14% discount to its net asset value. That’s a little pricier than its five-year average 17% discount to NAV, but it’s still the only place anyone can get Taiwan stocks this cheap right now.

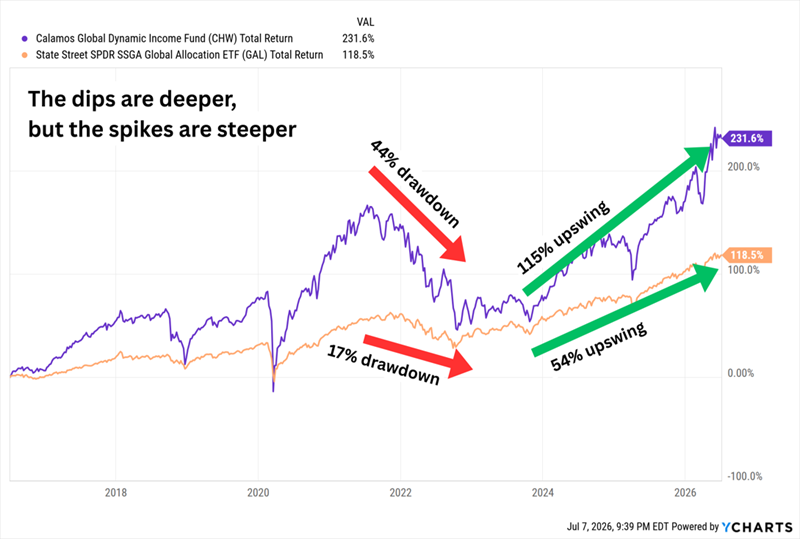

Calamos Global Dynamic Income Fund (CHW)Distribution Rate: 8.2%

Calamos Global Dynamic Income Fund (CHW) is a global allocation fund, which means it can invest in both equity and debt. The “dynamic” means management will shift the portfolio as market conditions change, so more than most funds, what they own today might not be what they own a year from now.

CHW’s portfolio is a wide umbrella–management is happy to own common stock, preferred stock, investment-grade corporates, junk, U.S. government bonds, convertible debt, asset-backed securities, bank loans and more. Right now, Calamos’ fund is 60% invested in common stock from both the U.S. and abroad, with a heavy tilt toward growth. Another 20% of assets are in convertibles, and the rest is spread among other fixed-income issues.

This CEF also uses a high amount of leverage (nearly 30%). That can be a double-edged sword depending on the market environment, but it has largely worked out for shareholders. The fund’s longer-term performance is certainly more volatile than similar plain-vanilla versions of the strategy–take, for instance, the SPDR SSGA Global Allocation ETF (GAL), which is in the same global moderate allocation category–but also more lucrative.

Iron-Stomached Investors Have Done Well in CHW

That leverage also helps pad a thick monthly dividend north of 8%.

Calamos Global Dynamic Income might be drawing up another peak, which would give some would-be investors pause. CHW nonetheless trades at a 9% discount to NAV–cheaper than its 7% five-year average–but the fund has offered up even steeper deals in the past.

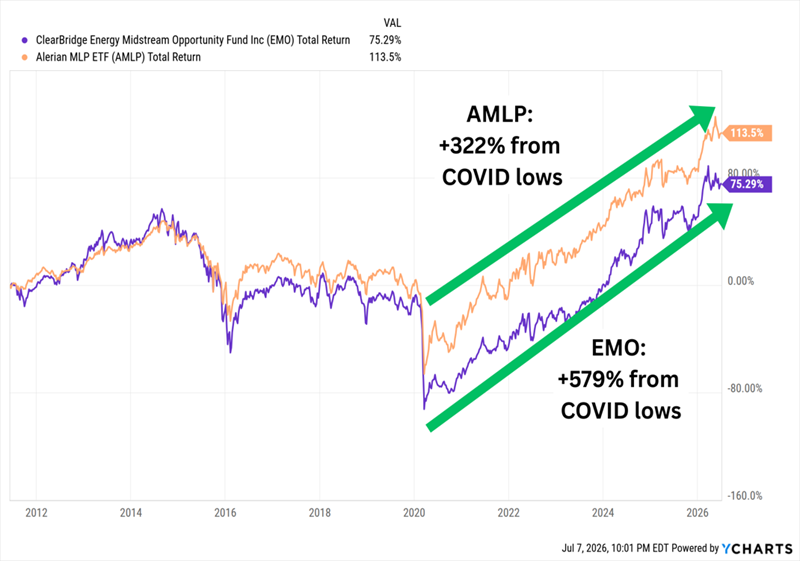

ClearBridge Energy Midstream Opportunity Fund (EMO)Distribution Rate: 8.5%

ClearBridge Energy Midstream Opportunity Fund (EMO) is a targeted play on the energy sector.

Co-Managers Peter Vanderlee and Patrick McElroy have compiled a tight portfolio of 20 companies operating in the energy “midstream” (pipelines, storage, terminals and other energy infrastructure assets). That means it owns master limited partnerships (MLPs) such as Energy Transfer LP (ET) and MPLX LP (MPLX), as well as traditional corporations such as Targa Resources (TRGP) and Williams Cos. (WMB).

This Franklin Templeton CEF has historically underperformed its benchmark, the Alerian MLP Index, since it came to life in 2011. But we can largely blame long down-to-flat periods for energy infrastructure broadly since then–during bull markets, EMO has let it rip, thanks in some part to moderate-to-high leverage (currently 20%, though I’ve seen it above 30% in the past).

EMO Can Be a Fair-Weather Fund. But That Works When the Weather Is Fair.

That same leverage also helps EMO squeeze out a percentage point or two more in yield out of its monthly distribution than energy infrastructure ETFs.

ClearBridge Energy Midstream Opportunity’s five-year average discount is a deep 13%, which is roughly where it sits today–nominally cheap, but fairly priced relative to its history.

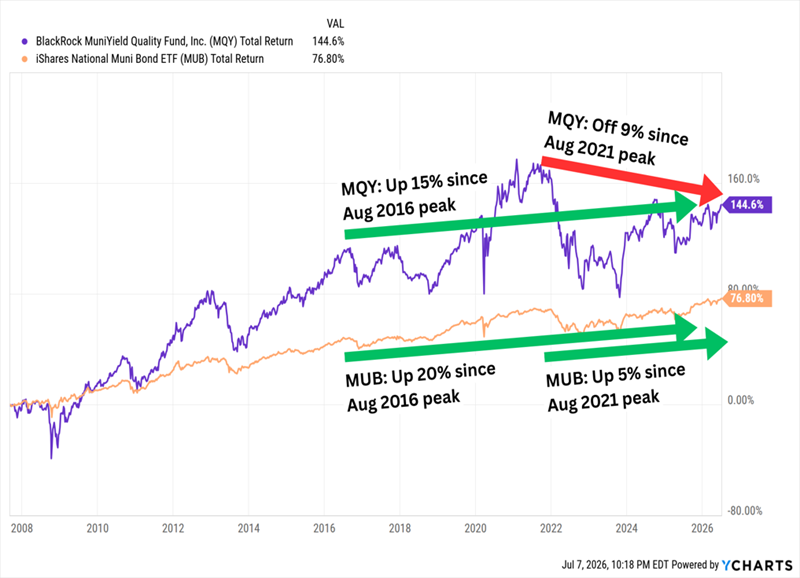

BlackRock Muniyield Quality (MQY)Distribution Rate: 6.0%

Municipal bond funds are truly “hidden yields.”

The BlackRock Muniyield Quality (MQY) yields 6%, paid monthly–slightly below what junk ETFs are offering. But those junk ETFs can’t offer what MQY does: a federal tax exemption.

To get an idea of how big a deal that is: Someone in the 37% tax bracket paying the 3.8% net investment income tax (NIIT) would need to buy a taxable bond fund paying 10.1% to get the same amount of take-home income as they’d earn from MQY!

And we’re not buying junk to get that sky-high tax-equivalent yield. Munibond funds are often high-quality to begin with, and MQY’s management is explicitly tasked with owning higher-graded debt. More than 85% of the portfolio’s assets are investment-grade in nature, and three-quarters is rated A or above.

Extremely high leverage north of 40% means we’re getting a much bumpier ride than a traditional bond fund, so we need to pick our spots and not look at performance every day–but over the long term, MQY has offered up the same rising tide as funds like iShares National Muni Bond ETF (MUB)–just better.

But Beware: Buying at Peaks Can Hobble Us

MQY isn’t running particularly hot right now, and its 8% discount is about a percentage point cheaper than its five-year average.

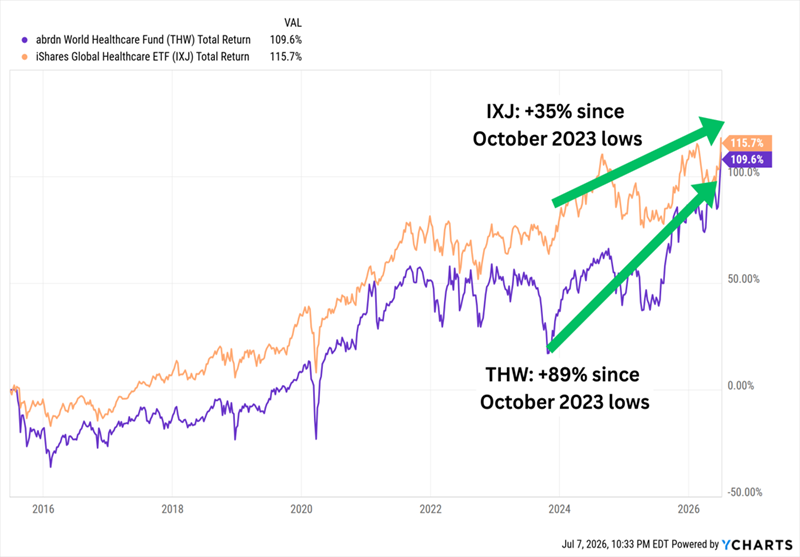

abrdn World Healthcare Fund (THW)Distribution Rate: 10.4%

Of all the CEFs I’m talking about today, abrdn World Healthcare Fund (THW) has the smallest discount right now, at just 4% to NAV–but it’s the best relative value.

Shares normally trade at a 4% premium.

We won’t find anything like this in ETF-land. We’ll start with its global nature–most ETFs that invest in the healthcare sector are heavy in U.S. companies, but only a handful are rich in international names. THW’s assets are split roughly 50/50 between American and foreign stocks, with most of the latter represented by western Europe.

We’re also going above and beyond traditional corporations. Yes, we have pharmaceuticals, biotech, life science and health insurers. But abrdn’s fund also holds healthcare real estate investment trusts (REITs), bonds, even venture capital. Toss in a decent amount of leverage (~20%) and a sky-high 10%-plus yield, and what do we get?

A Surprisingly Mixed Bag

THW has been much more productive of late, especially coming out of the 2023 downturn. But unlike the aforementioned EMO energy fund, abrdn’s CEF has largely existed in a healthcare bull market since inception in 2015–yet has failed to really stand out.

The culprit is management’s mix of debt and REITs–great for income, less great for growth.

Tired of Market Chaos? One of My Favorite 11% Dividend Is a ‘Cool’ Cure

Are you exhausted trying to keep up with the news lately? I don’t blame you–the news cycle is in overdrive, which means the market is a minefield of headline risk right now.

That’s why I always hold a few double-digit yielders. Massive income inflows can go a long way toward stabilizing our portfolios in turbulent markets while helping us come out ahead.

But only if we hold the right payers.

Longtime underperformers and funds with violent swings just won’t cut it.

When I take a swing on a double-digit yield, I look for highly skilled managers with a track record of running up the score on their competition.

Right now, one of my favorite home-run dividends is a heavily diversified, brilliantly built bond portfolio that yields 11% but is also set up for stock-like gains.

This fund checks off just about every income box I can think of:

- It pays a whopping 11% in annual income!

- It has increased its dividend over time

- It has paid out multiple special dividends

- And it pays its dividends each and every month!

And what about the fund’s manager? Morningstar previously named him a Fixed Income Manager of the Year, and he’s been inducted into the Fixed Income Analysts Society Hall of Fame.

That’s about as good a resume as we’ll find, and his fund will pay us $1,100 for every $10K we invest.

But the window is closing fast! Premiums on funds like these tend to rise as volatility ticks higher and as investors rotate out of growth stocks and into reliable sources of income like this. I don’t want you to miss your chance. Click here and I’ll introduce you to this incredible 11% payer and give you a free Special Report revealing its name and ticker.